Sign up

Highlights - 02/07/2020

Brazilian Scenario for 2020

Watch the full video

Market Monitoring - 02/07/2020

Metrics that help measure the effectiveness of the IR program

Measuring the efforts carried out by IR professionals has never been an easy task since data is rarely integrated. By analyzing share prices alone, we ignore issues that go beyond the work carried out by IR, thus compromising the result of the assessment. Additionally, the number of meetings or conferences held in the period does not necessarily imply they were effective. The challenge for Investor Relations Officers is to gain exposure to C-Level and Board executives in order to present the efforts carried out by the IR team aimed at:

(i) reducing cost of capital;

(ii) generating value by raising the ratio between share price upside and financial multiples (always in relation to the company’s peers);

(iii) managing the company’s shareholder based in such a way that it is in line with the company’s current investment strategy and thesis;

(iv) mastering relationship with analysts to reduce dispersion between estimates;

(v) measuring the conversion rate of prospect investors into actual shareholders as a result of meetings and conferences, thus improving the use of management’s time;

(vi) receiving feedback from the market on its perception regarding the company’s positioning and strategy against its peers and/or comparable players;

(vii) monitoring the company’s compliance with regulatory bodies;

(viii) articulating the company’s value proposition: create an investment thesis based on premises and facts that clearly expose the company’s strategic choices and how it effectively creates value through consistent and sustainable growth.

Highlights - 02/04/2020

Opening Panel with Roberto Sallouti, CEO of BTG Pactual

Highlights - 02/03/2020

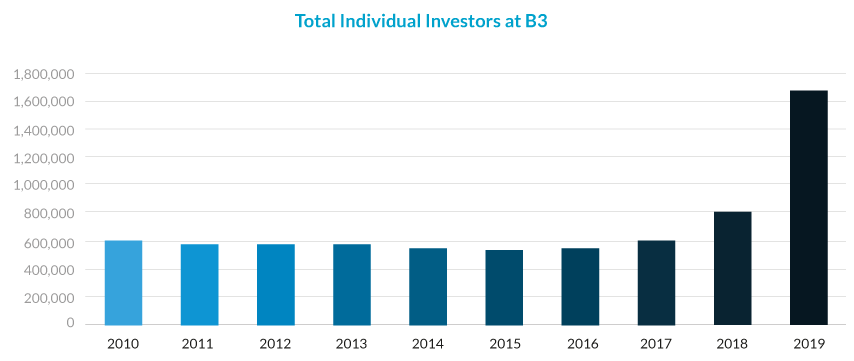

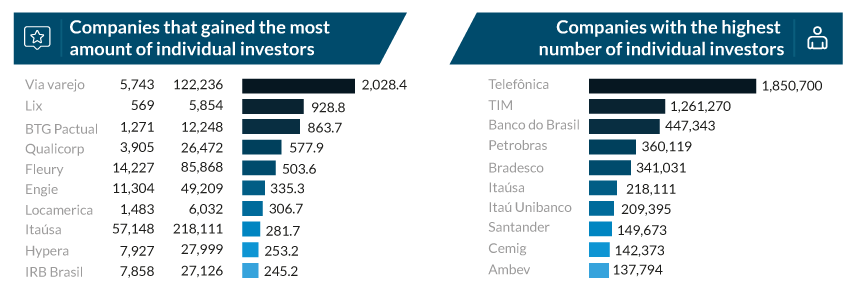

Communication with Individual Investors

The role played by Investor Relations has been quickly evolving, whether due to changes in regulation, new technologies or the dynamics of an unpredictable market. Having control over these transformations is fundamental for success.

To help keep you informed and, perhaps, even contribute with your annual planning, we elaborated a list of the key investor relations trends for 2020:

Given the scenario of lower interest rates in Brazil, new individual investors are entering the stock market. Therefore, companies now face the challenge of adapting its communication style in order to meet the demands of this growing audience, which totaled 1.7 million individuals in 2019.

In order to attract this new type of investor, IR professionals need to take steps beyond the traditional approach aimed at institutional investors, which includes invitations to events, access to management and an open communication channel with the IR department.

Individual investors have more dynamic profiles and seek for operating and financial data in a more digital and direct manner. They appreciate interactive solutions, such as videos, podcasts, social networks and intensive use of technological tools.

Thus, IR professionals need to establish a multichannel approach that ensures that the company’s message is being well understood by all investors.

Source: B3 and Reference Forms Publication: Valor Econômico

Market Monitoring - 10/17/2019

The exchanges, the issuers and the maker-takers

Two overarching topics were front and center during June’s 2019 NIRI Annual Conference. A great primer on environmental, social and corporate governance, or ESG, was written by my colleague, Mark Schwalenberg, CFA, in March. The second topic to garner attention was the Securities and Exchange Commission’s (SEC) pending Rule 610T of Regulation NMS, or Transaction Fee Pilot in NMS stocks. The purpose of this two-year pilot program is to test the effects of “maker-taker” fees on order routing and execution.

U.S. exchanges predominantly employ what is known as the “maker-taker” fee model which, put simply, incentivizes market makers to post buy and sell orders, thereby providing liquidity and increasing order flow in exchange for a transaction rebate. These are the “makers.” The other half of this model is comprised of the buying and selling contra-parties to the market markers, such as institutional investors, which are charged a fee for removing that liquidity. These are the “takers.” For this model to remain viable exchanges build in a spread, which they retain as transaction revenue, between rebates paid to the makers and fees charged to the takers.

The predominant criticism of maker-taker is that this system creates a potential conflict of interest among market makers and brokers to prioritize rebate fees over seeking the best trade execution. Although price priority is mandated by the SEC’s Order Protection Rule, this does not address market makers choosing to execute trades on one exchange over another based upon rebate fees when the best price is posted on multiple venues. Thus, best price does not take into account rebates and fees, resulting in potential distortion of market quality. An oft-cited 2013 research study performed by Robert Battalio and Shane Corwin, both of the University of Notre Dame’s Mendoza College of Business, and Robert Jenkins from Indiana University’s Kelley School of Business concluded that “several large retail brokerages route their order flow in a manner that appears to maximize order flow payments.”

This caught the attention, not only of the SEC, but lawmakers as well. After Senator Charles Schumer called for the SEC to study the issue in 2014, then-Commissioner Luis Aguilar confirmed the SEC was considering a pilot program to examine the trading of securities that retained the existing fee structure compared with those for which fees would be reduced or eliminated. In March 2018 current Chairman Jay Clayton announced that the SEC voted to propose a two-year Transaction Fee Pilot with an automatic sunset after the first year unless extended for a second year. As originally proposed the pilot program would have created three test groups of 1,000 stocks each, with fee caps of $0.0015 per share and $0.0005 per share, with no cap on rebates, and the third prohibiting rebates while still subject to Rule 610(c) which caps fees at $0.0030 per share. The control group would continue to be subject to Rule 610(c) fee cap and no cap on rebates.

Following the mandated 60 day comment period during which no less than 150 comments were received and numerous meetings held with market participants during and after the comment period, in December 2018 the SEC voted to adopt a revised version of the pilot program that applies to test group stocks traded on exchanges while exempting those same stocks when traded on off-exchange venues. The final version also reduced the number of test groups to two, each comprised of 730 stocks. Test Group 1 stocks would have a $0.0010 fee cap with no cap on rebates. Stocks in Test Group 2 would remain subject to the 610(c) $0.0030 fee cap while rebates would be prohibited. The control group, securities not in either test group, would remain subject to the 610(c) fee cap with no cap on rebates.

Exchanges have opposed both plans. One point of contention is that the increased cost of compliance for data collection and dissemination, and loss of fee revenue would result in those costs ultimately being born by the investor and make them less competitive relative to off-exchange venues such as alternative trading systems (ATS) and dark pools. Others include the potential for increased volatility and reduced liquidity. Additional concerns are that brokers may also lose revenue and incur increased costs to conform and that market makers will widen their spreads, all costs which would be incurred by investors. The NYSE estimated a $1 billion cost just from the initial pilot program proposal and $3.8 billion if those fee limits had been applied market-wide.

In February 2019 the New York Stock Exchange, Nasdaq and Cboe Global Markets filed lawsuits asking the District of Columbia Circuit Court of Appeals to find the pilot program rules unlawful. The NYSE’s petition argued that Rule 610T is unlawful under the Securities Exchange Act of 1934 as well as the Administrative Procedures Act. While the SEC has placed the rule on hold pending litigation, the agency said exchanges must still collect broker order routing data, needed as a baseline for the program, between July 1 and December 31 of 2019. Most recently, judges for a federal appeals court sharply questioned whether regulators worried about market fairness can require stock exchanges to experiment with the fees they charge.

While much of the debate over the effects of the pilot program has focused on the exchanges, market makers, brokers and investors, there is another group of market participants to be considered: the issuers. While the SEC has not released a list of stocks to be included in the program, issuers are apprehensive over how they would be affected should they be placed into one of the two test groups and there appears to be no opt-out provisions.

The exchanges and issuers have both argued that the SEC failed to analyze, or even consider, how the pilot program would affect issuers. Nasdaq’s comment letter stated that the pilot program would have an outsized negative affect on “small to medium issuers since exchanges will not be able to provide incentives to market makers to support trading in those companies’ securities.” The NYSE’s comment letter said that “transactions in those securities would be more expensive and less attractive to investors, which would negatively impact issuers’ ability to raise capital.” The NYSE’s web site also states that pilot program stocks would be disadvantaged due to wider spreads relative to other stocks, making an investment less appealing, and that a company whose stock is included in the pilot program would be required to provide a larger discount to market for any secondary offerings than would otherwise be needed due to wider spreads. Again, it is posited that this would provide competitors not included in the pilot program with a built-in advantage. Wider spreads, it is argued, will also result in higher costs for issuers conducting share repurchase programs. These were the messages delivered again and again in letters from issuers to the SEC during the comment period, revealing very real concerns regarding their stocks’ spreads and liquidity versus their competition, discounting of secondary capital raises and increased costs of share repurchase programs.

The question is whether, and if so, to what extent the anticipated negative effects on an issuer’s stock is realized. If your stock is not chosen for the pilot program, then it’s business as usual. If your stock is chosen for one of the test groups, then it will be a scramble to anticipate exactly how and to what degree you will be affected. If recent history is any guide one has only to look at the SEC’s previous effort, the Tick Size Pilot Program, and it is not encouraging. Implemented in October 2016 following pressure from lawmakers on Capitol Hill (sound familiar?), even after the SEC said it was unnecessary, as an effort to determine whether mandating a minimum $0.05 tick size in 1,200 test stocks with market caps below $3 billion resulted in an increase in liquidity along with an increase in all of the benefits that were supposed to follow. This two-year program was allowed to sunset after the first year. Actually, after receiving numerous requests, the SEC ended the program two days short of one year, having been called a waste of time and money by many. According to Barron’s, “The Tick Size Pilot Program that was supposed to revitalize trading liquidity, stock offerings, and job creation for small-cap public companies… resulted in stunted trading volumes in the nearly 1,200 stocks subjected to the two-year experiment, while also bloating investors’ trading costs by as much as $900 million.”

When, and in what form, the Transaction Fee Pilot will be implemented is still to be determined and could very well be decided, at least in part, as a result of the litigation undertaken by the three major exchanges. We could then be looking at a very different program if we are looking at one at all.

Larry W. Holub

Vice President, Capital Markets Intelligence